Since 2025, the price of sponge titanium has shown a significant upward trend, primarily due to the successful implementation of previous production cuts and inventory clearance measures. This trend has been further supported by domestic demand and chemical industry orders, as well as growth in overseas orders. Customs data indicates that China's sponge titanium exports reached 3,140 tonnes in the first half of 2025, representing a substantial year-on-year increase of 78%, reflecting the rapid expansion of overseas market demand.

Under the impetus of national supply-side reforms and environmental protection policies, semi-process production methods and outdated production capacity are gradually exiting the market, while leading companies are accelerating their transition to full-process production, resulting in a continuous increase in the concentration of China's sponge titanium industry. It is worth noting that there are significant price differences among enterprises for sponge titanium of different grades. This primarily stems from the differentiation in downstream titanium material orders—enterprises with higher prices primarily target the high-end sponge titanium market, while those with lower prices focus on supplying the mid-to-low-end market. This differentiated pricing strategy also constitutes a competitive advantage for China's sponge titanium in the international market.

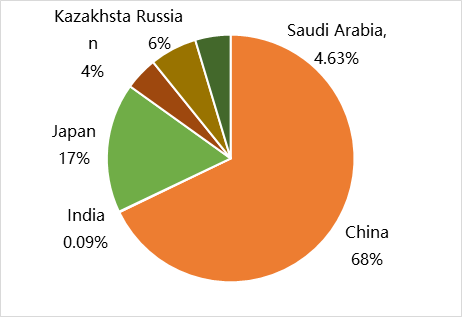

In terms of global production share, China accounts for 68% of the world's total sponge titanium production, firmly maintaining its position as the global leader. However, feedback from export markets indicates that Japan remains a significant competitor in the Asian market, with its sponge titanium industry dominated by Dongbang Titanium Industry and Osaka Titanium Industry Technology, which focus on the high-end order market. It is reported that Dongbang Titanium Industry has recently continued to expand its production capacity, further solidifying Japan's global leadership in the high-end sponge titanium sector. In contrast, China still lags behind in terms of advanced sponge titanium production technology. The Russian sponge titanium market is experiencing a significant decline. Due to the Russia-Ukraine conflict, the country has lost a large number of international orders, leading to severe oversupply of sponge titanium and titanium ingot products. Currently, these accumulated inventories are primarily entering the Chinese market through trade channels, but the absorption process is progressing slowly.

According to domestic manufacturers, European customers generally prefer Grade 0 sponge titanium, but each order has different product requirements, making it difficult to establish a unified standard. Additionally, there are significant differences in price, payment terms, and delivery schedules, though overall quality requirements are stringent. The European supply chain is highly fragmented, with limited domestic smelting capacity and significant differences in demand among manufacturers. In contrast, the American supply chain is more complete, but export difficulties are significant due to tariff barriers. Southeast Asian customers primarily purchase lower-grade sponge titanium such as Grade 2, but they exert significant pressure to lower prices, resulting in relatively limited export profit margins.

Looking ahead to the prospects for Chinese sponge titanium exports, the civilian chemical sector is expected to become an important growth area. Against the backdrop of continuously increasing domestic production capacity, expanding overseas markets will become an important channel for absorbing excess capacity. In the future, it will be necessary to establish a more comprehensive export mechanism to promote healthy market development. SMM will continue to monitor and promptly update price dynamics in overseas sponge titanium markets.